When it comes to filing IRS Form 8832, it’s essential to understand which businesses are eligible and the various tax classification choices available. This form serves as your gateway to determining whether your business will be taxed as a C-corporation, a partnership, or a sole proprietorship. Let’s break it down.

Which Businesses Qualify for IRS Form 8832

When it comes to maximizing tax savings for your small business, navigating the complexities of tax classifications is paramount. The IRS Form 8832, aptly named the “Entity Classification Election,” is your ticket to gaining control over how your business is classified for federal tax purposes. Without this essential form, your business risks default tax classification, which could significantly impact your tax liability.

Changing your tax election status using Form 8832 has the potential to save your business thousands of dollars annually in taxes. Additionally, it empowers your business to alter its tax status, allowing you to report income and expenses directly on your business tax return, rather than having owners report them on their individual tax returns. In this comprehensive guide, we will walk you through how to complete IRS Form 8832, answering frequently asked questions along the way. Get ready to harness the full potential of this valuable tax tool!

Eligible Businesses

Only specific business entities can utilize IRS Form 8832 to select their preferred tax status. These eligible entities include U.S.-based partnerships, U.S.-based limited liability companies (LLCs), and certain foreign entities. Here’s how this form can impact them:

Limited Liability Companies (LLCs)

LLCs are a common entity that often leverage IRS Form 8832 to modify their tax classification. By default, a single-member LLC is considered a disregarded entity for tax purposes, while a multi-member LLC is categorized as a partnership.

Single-Member LLCs: These entities have the option to complete Form 8832 to change their tax status to a C-corporation, partnership, or sole proprietorship. Without this form, single-member LLCs are automatically treated as sole proprietorships for tax purposes.

Multi-Member LLCs: Similar to their single-member counterparts, multi-member LLCs can utilize Form 8832 to elect to be taxed as a C-corporation, partnership, or sole proprietorship. Failing to submit this form will result in multi-member LLCs being taxed as partnerships.

Note on S-Corporation Status

If your intention is to be taxed as an S-corporation, it’s crucial to understand that Form 8832 won’t serve this purpose. Instead, you’ll need to file a separate document, IRS Form 2553, to achieve S-corporation tax status.

By understanding these options, you can make informed decisions that align with your business goals and financial strategy.

Impact of Not Filing Form 8832

What occurs when you decide not to submit Form 8832? The Internal Revenue Service (IRS) will assign your business a default tax classification, and this choice may significantly impact your tax liabilities. However, there are specific scenarios where you may opt not to file IRS Form 8832.

Sticking with Default Tax Status

If you are content with the default tax classification provided by the IRS and it aligns with your business objectives, there’s no obligation to file Form 8832. This form primarily serves businesses seeking to make deliberate changes to their tax status.

Important Note on Corporate Taxation

For those contemplating corporate taxation, it’s essential to understand the process. Before filing IRS Form 8832, you must first complete the formal step of filing articles of incorporation with your secretary of state. Once this step is successfully completed, you can then proceed to submit Form 8832 to achieve your desired tax status.

While not every business needs to file IRS Form 8832, it’s crucial to make an informed decision regarding your tax classification. Understanding the implications of default tax status and the prerequisites for specific tax elections will empower you to navigate the taxation landscape effectively.

Gathering the Necessary Details for Form 8832

To complete IRS Form 8832, gather the following essential information:

- Business Details

- Business Name

- Business Address

- Business Phone Number

- Employer Identification Number (EIN)

- The EIN serves as the tax identification number for your business.

- Single Owner Details

- If your business has only one owner, provide the following:

- Owner’s Name

- Owner’s Social Security Number or other “identifying” number

Demystifying IRS Form 8832: Step-by-Step Directions

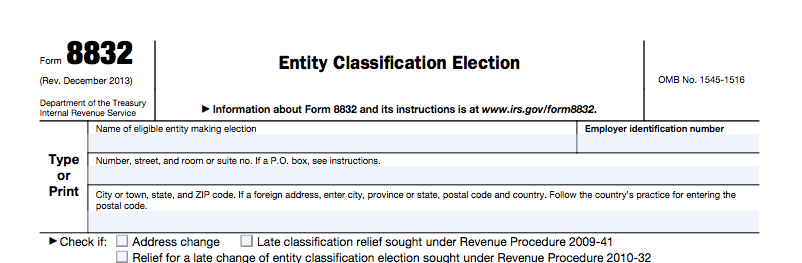

IRS Form 8832 is available for download on the official IRS website. The initial page of the form provides essential instructions, including mailing details for your tax forms. The actual form starts on page two. While manually filling out the form is an option, it may increase the risk of errors. Therefore, it is advisable to submit the form electronically for accuracy and efficiency.

In this section, you will be required to furnish basic information about your business:

- Business Name: Enter your full business name as it appears in official records.

- Business Address: Provide your current business address.

- Employer Identification Number (EIN): Include your EIN, which serves as your business’s unique tax identification number.

If you haven’t obtained an EIN yet, you can conveniently apply for an Employer Identification Number online. In case you possess an EIN but can’t recall it, refer to the EIN confirmation letter sent to you by the IRS when you initially applied. Alternatively, you can locate this number on previous tax returns or within your business permits and licenses.

If you’ve recently changed your business address following the filing of Form SS-4 or your most recent tax returns, please select the “Address change” option. If you forgot to file the necessary form but wish to apply the change retroactively to prior tax years, mark the “Late classification relief…” box accordingly. This ensures that your updated information is appropriately reflected in previous tax records.

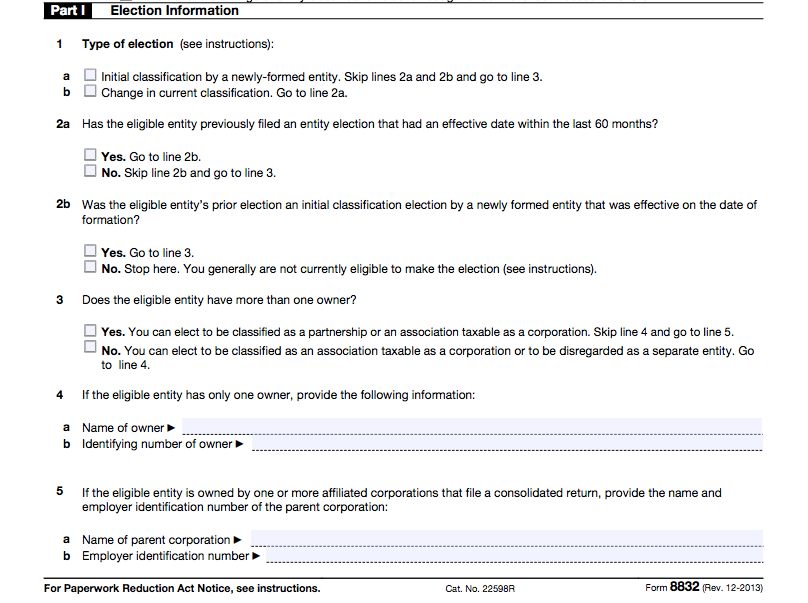

Complete part 1, election information

In Part 1 of IRS Form 8832, you’ll encounter a set of questions related to your tax status election. It’s essential to note that you may not need to answer every question, as your specific situation determines which sections apply to you.

Line 1: Election Type

- Line 1(a) – If you are making your initial tax status change, select this option.

- Line 1(b) – If this is not your first tax status change, you should complete lines 2a and 2b, providing details about the timing of your last election. Typically, the IRS imposes restrictions on changing your tax classification within a 60-month period. However, if your previous election coincided with your business’s formation date and became effective immediately upon formation, the 60-month limit does not apply.

Line 3: Number of Owners

Proceed to Line 3 if you have selected option “a” in Line 1. Here, you will specify whether your business has multiple owners. Different tax status options are available based on your response.

- Sole Owner: If you are the sole owner, you can elect to be taxed as a disregarded entity or a C-corporation, and you will move on to Line 4.

- Multiple Owners: If your business has more than one owner, your choices include classification as a partnership or C-corporation. After indicating that your business has multiple owners, continue to Line 5. Here, you will provide the names and EINs of any parent corporations, if applicable.

This section of the form is pivotal in determining your business’s tax status, so ensure that you accurately complete the relevant lines based on your specific ownership structure and election type.

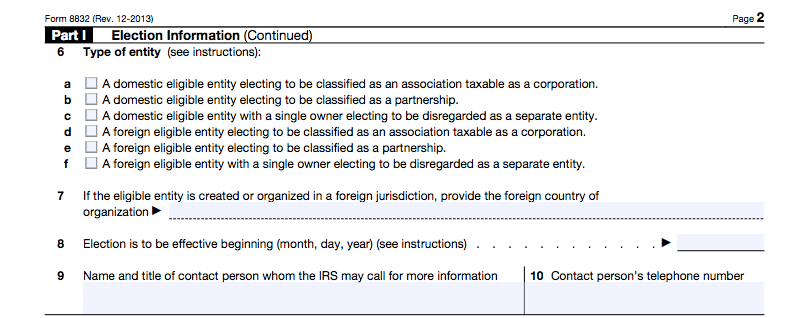

Line 6: Select Your Desired Tax Status

Line 6 is a crucial step where you will choose the tax status that aligns with your business’s needs and goals. Your selection here will determine how your business will be taxed going forward.

Line 7: Foreign Entity Information (Foreign Entities Only)

For foreign entities filing IRS Form 8832, Line 7 is where you’ll provide the name of the foreign country of organization. If your business is not a foreign entity, you can skip this line.

Line 8: Effective Date of Tax Status Change

On Line 8, specify the exact date you wish your new tax status to take effect. It’s important to note that there are some limitations regarding this date:

- You cannot choose a date that is more than 75 days before the filing date of the form.

- The selected date should not be more than 12 months after the filing date.

- If you do not provide a date on Line 8, the IRS will automatically consider the filing date as the effective date.

Lines 9 and 10: Contact Information

Lastly, on Lines 9 and 10, furnish the name and title of an individual whom the IRS may contact for any additional information related to your tax status election. Additionally, provide a valid phone number to ensure effective communication.

Completing these lines accurately ensures that your tax status change is properly documented and helps prevent any delays or misunderstandings with the IRS.

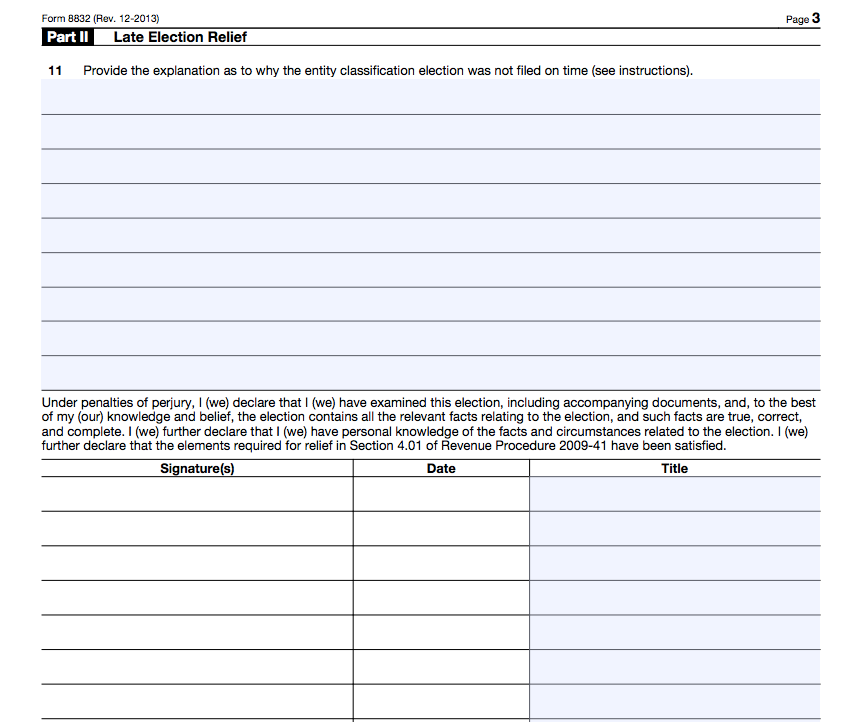

Complete part 2, If Seeking Late Election Relief

Part 2 of IRS Form 8832 is dedicated to those who need to file their entity classification election past the standard deadline. If you find yourself in this situation, there’s still an opportunity to seek late election relief. However, certain criteria must be met to be eligible for this relief:

- You failed to obtain your desired tax classification because you did not file Form 8832 within the initial timeframe.

- You have not yet filed your tax returns since the tax deadline has not passed, or you filed your taxes on time.

- You can provide a reasonable cause that explains why you were unable to file Form 8832 within the original deadline.

- Your request for late election relief falls within a specific window of three years and 75 days from your requested effective date.

If you meet these eligibility requirements, use Part 2, Line 11, to provide a comprehensive explanation of your circumstances and the reasonable cause for the delay in filing Form 8832. Additionally, this is where you will affix your signature to certify your submission.

Successfully navigating Part 2 and meeting these criteria will allow you to request late election relief effectively, ensuring your business’s tax classification aligns with your current needs.

Next Step: Mail IRS Form 8832

Once you’ve diligently completed and signed IRS Form 8832, the next step is to mail it to the appropriate office. The specific mailing address depends on your business’s location, and you can find this address on the first page of the Form 8832 PDF.

To ensure your submission is valid, you’ll need acceptable proof of filing. This can include:

- A certified or registered mail receipt from the United States Postal Service.

- Form 8832 with an accepted stamp.

- The form with a stamped IRS received date.

- An IRS letter confirming the acceptance of the form.

Now, let’s identify the correct mailing address for your location:

For Taxpayers in: Connecticut, Delaware, Washington D.C., Georgia, Illinois, Indiana, Kentucky, Maine, Maryland, Massachusetts, Michigan, New Hampshire, New Jersey, New York, North Carolina, Ohio, Pennsylvania, Rhode Island, South Carolina, Vermont, Virginia, West Virginia, and Wisconsin, you will mail your Form 8832 to:

Department of the Treasury

Internal Revenue Service Center

Kansas City, MO 64999

For Taxpayers in: Alabama, Alaska, Arizona, Arkansas, California, Colorado, Florida, Hawaii, Idaho, Iowa, Kansas, Louisiana, Minnesota, Mississippi, Missouri, Montana, Nebraska, Nevada, New Mexico, North Dakota, Oklahoma, Oregon, South Dakota, Tennessee, Texas, Utah, Washington, and Wyoming, your Form 8832 should be mailed to:

Department of the Treasury

Internal Revenue Service Center

Ogden, UT 84201

Ensuring you send your Form 8832 to the correct address and retain proof of filing will help facilitate the tax classification change process for your business.

Final Step: Monitor Your Mail and IRS Response

Once you’ve submitted your Form 8832, it’s essential to stay vigilant regarding any correspondence from the IRS. Typically, the IRS will make a determination regarding your Form 8832 filing within 60 days. They will send their decision letter to the address you provided during the form’s completion.

If this 60-day period passes without any communication from the IRS, it’s advisable to take proactive measures. You can either call the IRS directly at 1-800-829-0115 to inquire about the status of your Form 8832, or you can opt to send a written inquiry to the appropriate service center.

By monitoring your mail and promptly addressing any potential delays or issues, you’ll ensure that your business’s tax classification change proceeds smoothly.

When to File Form 8832: Key Considerations

Unlike many tax-related forms that come with strict deadlines, Form 8832 provides business owners with the flexibility to file at various stages of their business journey. You can submit it right at the inception of your business or at any point during your business’s existence.

However, it’s crucial to understand the significance of the filing date. The tax status of your business can be affected based on when you file:

- Up to 75 Days Before Filing: Your chosen tax classification can take effect retroactively for a period of up to 75 days before the actual filing date.

- Up to One Year After Filing: Alternatively, you can opt for your tax status change to apply up to one year after you submit Form 8832.

In cases where you leave the effective date field blank on the form, the filing date itself will be considered the effective date. Therefore, selecting the appropriate date for your desired tax classification to commence is pivotal. Consulting with your accountant is advisable, as they can provide guidance on selecting the most advantageous effective date based on your business type and specific circumstances. This strategic decision could impact your tax situation positively.

Crucial Considerations for Established Businesses

Form 8832 can be filed at any stage in your business’s lifecycle. Partnerships and LLCs, in particular, may find value in submitting this form if they haven’t done so previously or if they initially filed as a corporation.

However, it’s crucial to note that there are limitations on how frequently you can change your tax status – generally every five years. Exceptions do exist, though, and consulting with your accountant can help determine if your business qualifies for one of these exceptions.

Now, when it comes to affiliates, it’s essential to address the issue of tax consistency. Part I, Line 5 of the form inquires whether your business is owned by one or more parent affiliated (or parent) companies that file a consolidated tax return. If this applies to your situation, provide the parent company’s name and its EIN number. This step ensures that affiliated companies are taxed appropriately and in alignment with the consolidated return.

It’s also worth mentioning that certain entities established outside of the United States or in specific U.S. territories are eligible to complete IRS Form 8832. You can find the list of these eligible locations on the form’s seventh page.

Form 8832 FAQs: Your Tax Election Questions Answered

Here, we’ve compiled a list of frequently asked questions (FAQs) regarding IRS Form 8832. While we aim to provide comprehensive answers, it’s essential to remember that the IRS and your accountant remain excellent resources for any specific inquiries or clarifications.

As always, consult a qualified tax advisor if you’re unsure whether to change your tax classification. That person can guide you through the ins and outs of this form — and whether changing your tax status is the right move for your business in the first place.